On the current UK government immigration policy white paper respondents reported:

- 28% are reliant on EU nationals in the workforce

- 62% see the potential salary cap of £30k as unacceptable

- 69% believe policy should allow regional variation to UK immigration policy to address Scotland’s unique population needs

- 33% do not agree that the current sponsorship is efficient and cost effective to business

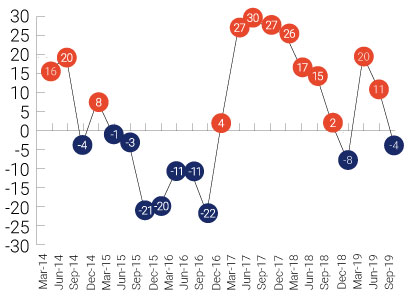

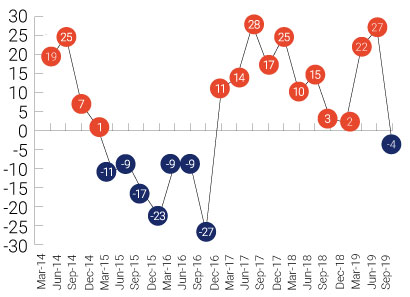

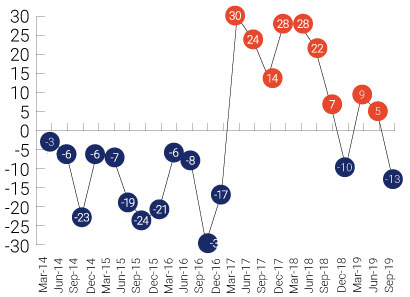

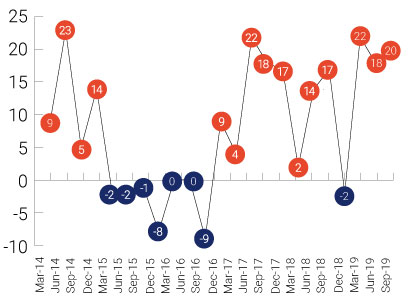

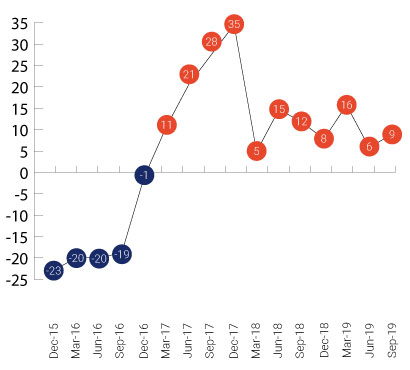

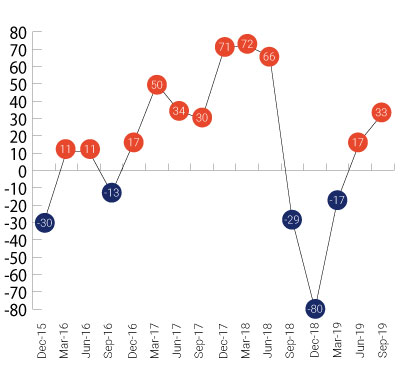

Annual Trends

Most indicators have dipped since last quarter. Order intake has fallen after two positive quarters, and output volume is negative for the first time since September 2016.

Export levels are negative for the first time this year.

Contrary to these trends, staffing levels still show a positive intention and have risen slightly this quarter, and this is felt to be due to open vacancies intended to be filled.

Order Intake

Output Volume

Exports

Staffing

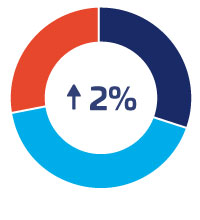

Net | Up | Same | Down | |

UK Orders | 2% | 30% | 42% | 28% |

Small companies | 5% | 35% | 35% | 30% |

Medium companies | 8% | 25% | 58% | 17% |

Large companies | -33% | 17% | 33% | 50% |

Machine shops | 0% | 33% | 34% | 33% |

Mechanical equipment | 9% | 36% | 37% | 27% |

Metal manufacturing | -60% | 0% | 40% | 60% |

Non-metal products | -14% | 14% | 57% | 29% |

Fabricators | 17% | 42% | 33% | 25% |

Electronics | 16% | 33% | 50% | 17% |

UK orders remain positive, with the balance of change at 2% (8% lower than last quarter). Small and medium sized companies are positive, but large companies have fallen into negative territory. Within the sectors mechanical equipment, fabricators and electronics are all reporting positive returns. Machine shops have equal numbers of companies reporting increases and decreases; and metal manufacturing and non-metal products are reporting negative figures.

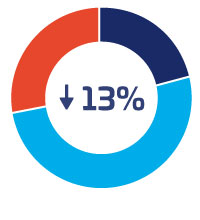

Net | Up | Same | Down | |

Export Orders | -13% | 26% | 35% | 39% |

Small companies | -5% | 30% | 35% | 35% |

Medium companies | -29% | 17% | 37% | 46% |

Large companies | 17% | 50% | 17% | 33% |

Machine shops | 0% | 25% | 50% | 25% |

Mechanical equipment | 14% | 43% | 28% | 29% |

Metal manufacturing | -75% | 0% | 25% | 75% |

Non-metal products | -50% | 0% | 50% | 50% |

Fabricators | -50% | 0% | 50% | 50% |

Electronics | 0% | 40% | 20% | 40% |

Export orders are negative for small and medium companies, and positive for large companies. The balance of change is -5% for small companies, -29% for medium companies, and 17% for large companies. In the sectors, mechanical equipment is positive; metal manufacturing, non-metal products and fabricators are negative; and machine shops and electronics have a similar number of companies reporting increases and decreases.

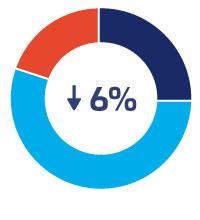

Net | Up | Same | Down | |

Optimism | -6% | 21% | 51% | 28% |

Small companies | -6% | 23% | 48% | 29% |

Medium companies | -8% | 19% | 54% | 27% |

Large companies | 0% | 17% | 66% | 17% |

Machine shops | 33% | 50% | 33% | 17% |

Mechanical equipment | 0% | 20% | 60% | 20% |

Metal manufacturing | -60% | 0% | 40% | 60% |

Non-metal products | -29% | 14% | 43% | 43% |

Fabricators | -8% | 25% | 42% | 33% |

Electronics | -16% | 17% | 50% | 33% |

Optimism is negative for the first time since September 2016. Small and medium companies are reporting decreases and large companies are reporting equal numbers of increases and decreases. In the various sectors machine shops are positive; mechanical equipment is reporting equal numbers of increases and decreases; metal manufacturing, non-metal products, fabricators and electronics are reporting decreases in optimism.

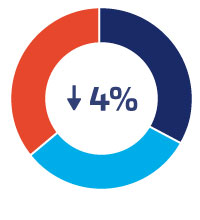

Net | Up | Same | Down | |

Output volume | -4% | 33% | 31% | 36% |

Small companies | -9% | 31% | 27% | 42% |

Medium companies | 12% | 38% | 35% | 27% |

Large companies | -16% | 17% | 50% | 33% |

Machine shops | -17% | 33% | 17% | 50% |

Mechanical equipment | -12% | 28% | 32% | 40% |

Metal manufacturing | -40% | 20% | 20% | 60% |

Non-metal products | -28% | 29% | 14% | 57% |

Fabricators | 0% | 33% | 34% | 33% |

Electronics | 16% | 33% | 50% | 17% |

Output volume is negative after 11 positive quarters, with small and large companies reporting decreases, and medium companies reporting an increase. Across the sectors electronics are positive; machine shops, mechanical equipment, metal manufacturing and non-metal products are negative; and fabricators are reporting equal numbers of increases and decreases.

Net | Up | Same | Down | |

Staffing | 20% | 39% | 42% | 19% |

Employees | ||||

Small companies | 19% | 35% | 48% | 17% |

Medium companies | 27% | 42% | 43% | 15% |

Large companies | 0% | 50% | 0% | 50% |

Machine shops | 0% | 83% | 17% | 0% |

Mechanical equipment | 28% | 44% | 40% | 16% |

Metal manufacturing | -20% | 0% | 80% | 20% |

Non-metal products | 0% | 29% | 42% | 29% |

Fabricators | 8% | 25% | 58% | 17% |

Electronics | -33% | 0% | 67% | 33% |

Employees

Employee numbers are positive for small and medium companies, and large companies are reporting equal numbers of increases and decreases. Mechanical equipment and fabricators have increased; metal manufacturing and electronics companies have reported decreases, and machine shops and non-metal products have reported equal numbers of increases and decreases.

Overtime -3% 26% 45% 29%

Overtime working continues in an increasing direction for small companies, whilst medium companies have fallen to a negative position, and large companies are even.

Net | Up | Same | Down | |

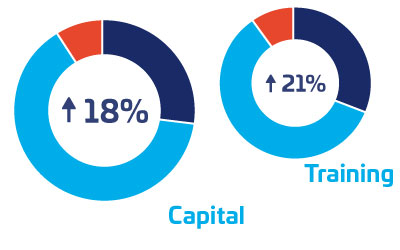

Investment | 18% | 27% | 64% | 9% |

Capital investment | ||||

Small companies | 8% | 23% | 62% | 15% |

Medium companies | 31% | 31% | 69% | 0% |

Large companies | 50% | 50% | 50% | 0% |

Machine shops | 50% | 67% | 16% | 17% |

Mechanical equipment | 30% | 30% | 70% | 0% |

Metal manufacturing | -20% | 0% | 80% | 20% |

Non-metal products | 14% | 43% | 28% | 29% |

Fabricators | 9% | 17% | 75% | 8% |

Electronics | 17% | 17% | 83% | 0% |

Investment

Capital investment plans have maintained similar positive levels to last quarter – all sizes of companies are positive. Within the sectors machine shops, mechanical equipment, non-metal products, fabricators and electronics are positive; and metal manufacturing is negative.

Training investment 21% 31% 59% 10%

Training investment plans have fallen slightly since last quarter, but all sizes of company are continuing to report positive figures.

Capacity Utilisation

Remains positive, at an improved level, for the eleventh consecutive quarter.

Forecast

Forecasts for the next three months are more positive than last quarter. In general, UK orders, export orders and output volume are forecast to pick up. Small and medium companies are forecasting positive figures for most measurements. Large companies are forecasting decreases in UK order intake and employee numbers.

Non-metal products, fabricators, machine shops and mechanical equipment are forecasting that the next quarter will be better than the previous. Metal manufacturing are expecting decreases in UK order intake, exports and output volume; and electronics are forecasting a decrease in exports orders and prices.

| Net | Up | Same | Down | |

Orders | 7% | 30% | 47% | 23% |

UK Orders | 5% | 28% | 49% | 23% |

Export Orders | 5% | 24% | 57% | 19% |

Output Volume | 12% | 36% | 40% | 24% |

Balance of change %

| Order Intake UK | Orders Export | Prices UK | Prices Export | Output Volume | Employees | |

|---|---|---|---|---|---|---|

| Small | 4 | 3 | 17 | 18 | 13 | 21 |

| Medium | 13 | 0 | 13 | 12 | 12 | 8 |

| Large | -17 | 33 | 33 | 17 | 17 | -17 |

| Metal manufacturing | -40 | -75 | 20 | 25 | -40 | 0 |

| Non-metal products | 29 | 0 | 14 | 17 | 14 | 0 |

| Electronics | 0 | -40 | 0 | -20 | 0 | 0 |

| Fabricators | 25 | 17 | 17 | 0 | 25 | 25 |

| Machine Shops | 17 | 0 | 17 | 0 | 17 | 33 |

| Mechanical Equipment | 18 | 23 | 27 | 27 | 24 | 20 |