Key highlights from this quarter:

- UK orders fall 18% from prior quarter to -16%

- Export orders fall further 3% to -16%

- Training investment falls 3% to +18%

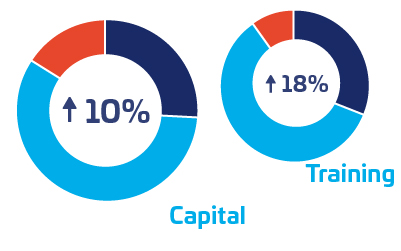

- Capital investment remains strong at +10% reflected in >50% of respondents planning new or enhanced ERP projects next year

Most indicators have dipped last quarter, with order intake and exports falling further since in this period. Staffing levels have dipped but are still positive.

Contrary to these trends, output volume has risen slightly this quarter, and this is assumed to be inventory building to offset uncertainty.

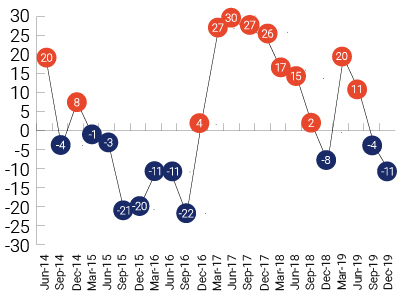

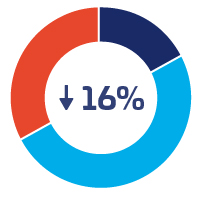

Order intake

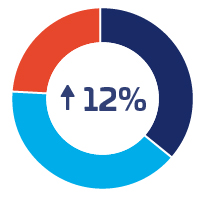

Output volume

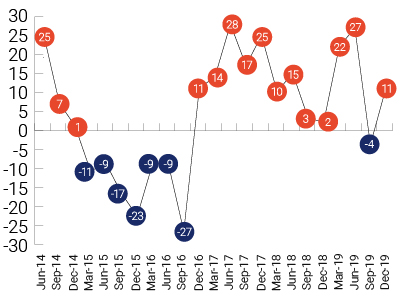

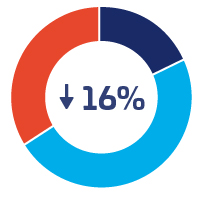

Exports

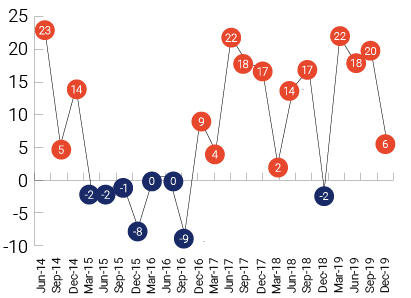

Staffing

Net | Up | Same | Down | |

UK Orders | -16% | 17% | 50% | 33% |

Small companies | -24% | 15% | 46% | 39% |

Medium companies | -4% | 20% | 56% | 24% |

Large companies | 25% | 25% | 75% | 0% |

Machine shops | -38% | 25% | 12% | 63% |

Mechanical equipment | -12% | 13% | 62% | 25% |

Metal manufacturing | -12% | 13% | 62% | 25% |

Non-metal products | -15% | 14% | 57% | 29% |

Fabricators | -8% | 15% | 62% | 23% |

Electronics | -50% | 17% | 16% | 67% |

UK orders are negative, with the balance of change at -16% (18% lower than last quarter). Small and medium sized companies are negative, and large companies have swung into positive territory. All sectors are reporting negative returns.

Net | Up | Same | Down | |

Export Orders | -16% | 18% | 48% | 34% |

Small companies | -16% | 18% | 48% | 34% |

Medium companies | -30% | 9% | 52% | 39% |

Large companies | 75% | 75% | 25% | 0% |

Machine shops | -33% | 0% | 67% | 33% |

Mechanical equipment | -14% | 18% | 50% | 32% |

Metal manufacturing | -14% | 29% | 28% | 43% |

Non-metal products | -33% | 0% | 67% | 33% |

Fabricators | -14% | 0% | 86% | 14% |

Electronics | -60% | 20% | 0% | 80% |

Export orders are negative for small and medium companies, and positive for large companies. The balance of change is -16% for small companies, -30% for medium companies, and 75% for large companies. All sectors are reporting negative returns.

Net | Up | Same | Down | |

Optimism | -5% | 24% | 47% | 29% |

Small companies | -9% | 23% | 45% | 32% |

Medium companies | -8% | 19% | 54% | 27% |

Large companies | 75% | 75% | 25% | 0% |

Machine shops | 0% | 38% | 24% | 38% |

Mechanical equipment | 4% | 24% | 56% | 20% |

Metal manufacturing | -13% | 25% | 37% | 38% |

Non-metal products | -57% | 14% | 15% | 71% |

Fabricators | 0% | 23% | 54% | 23% |

Electronics | -16% | 17% | 50% | 33% |

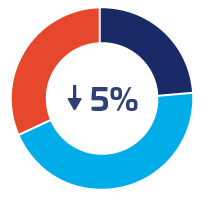

Optimism remains negative but is 1% point higher than last quarter. Small and medium companies are reporting decreases and large companies are reporting an increase. In the various sectors mechanical equipment is positive; machine shops and fabricators are reporting equal numbers of increases and decreases; metal manufacturing, non-metal products and electronics are reporting decreases in optimism.

Net | Up | Same | Down | |

Output volume | 12% | 36% | 40% | 24% |

Small companies | 7% | 35% | 37% | 28% |

Medium companies | 23% | 38% | 47% | 15% |

Large companies | 0% | 25% | 50% | 25% |

Machine shops | 0% | 38% | 24% | 38% |

Mechanical equipment | 8% | 32% | 44% | 24% |

Metal manufacturing | -37% | 13% | 37% | 50% |

Non-metal products | 14% | 43% | 28% | 29% |

Fabricators | 0% | 23% | 54% | 23% |

Electronics | 50% | 67% | 16% | 17% |

Output volume is positive for small and medium companies and large companies are reporting equal numbers of increases and decreases. Across the sectors mechanical equipment, non-metal products and electronics are positive; metal manufacturing is negative; and machine shops and fabricators are reporting equal numbers of increases and decreases.

Net | Up | Same | Down | |

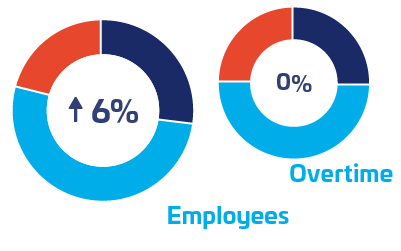

Staffing | 6% | 27% | 52% | 21% |

Small companies | 8% | 28% | 52% | 20% |

Medium companies | 4% | 23% | 58% | 19% |

Large companies | -25% | 25% | 25% | 50% |

Machine shops | 25% | 38% | 49% | 13% |

Mechanical equipment | -4% | 28% | 40% | 32% |

Metal manufacturing | 25% | 38% | 49% | 13% |

Non-metal products | -14% | 14% | 57% | 29% |

Fabricators | -7% | 8% | 77% | 15% |

Electronics | 0% | 17% | 66% | 17% |

Employees

Employee numbers are positive for small and medium companies, and negative for large companies. Machine shops and metal manufacturing have increased; mechanical equipment, non-metal products and fabricators have reported decreases, and electronic companies have reported equal numbers of increases and decreases.

Net | Up | Same | Down | |

Overtime | 0% | 25% | 50% | 25% |

Small companies | -8% | 21% | 50% | 29% |

Medium companies | 16% | 32% | 52% | 16% |

Large companies | 25% | 50% | 25% | 25% |

Overtime working continues in an increasing direction for medium and large companies, whilst small companies have fallen to a negative position.

Net | Up | Same | Down | |

Investment | 10% | 26% | 58% | 16% |

Small companies | 5% | 23% | 59% | 18% |

Medium companies | 11% | 23% | 65% | 12% |

Large companies | 75% | 75% | 25% | 0% |

Machine shops | 12% | 25% | 62% | 13% |

Mechanical equipment | -4% | 16% | 64% | 20% |

Metal manufacturing | 0% | 25% | 50% | 25% |

Non-metal products | 15% | 29% | 57% | 14% |

Fabricators | 8% | 23% | 62% | 15% |

Electronics | 17% | 17% | 83% | 0% |

Investment

Capital investment plans remain positive, although they have fallen slightly since last quarter. Within the sectors machine shops, non-metal products, fabricators and electronics are positive; mechanical equipment is negative; and metal manufacturing are reporting equal numbers of increases and decreases.

Net | Up | Same | Down | |

Training investment | 18% | 30% | 58% | 12% |

Small companies | 16% | 31% | 54% | 15% |

Medium companies | 15% | 23% | 69% | 8% |

Large companies | 75% | 75% | 25% | 0% |

Training investment plans have fallen slightly since last quarter, but all sizes of company are continuing to report positive figures.

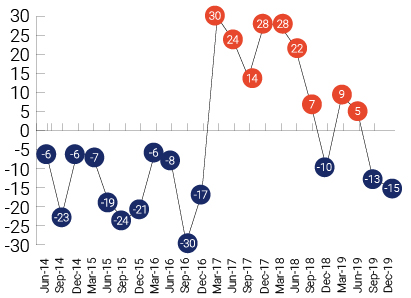

Capacity Utilisation

Capacity utilisation has fallen into negative territory for the first time since December 2016.

Fabricators

Order intake total Fabricators order intake has dropped since last quarter, and is now negative, returning to levels not seen since early 2018.

Forecast

Forecasts for the next three months are similar to last quarter. In general, UK orders and output volume are forecast to pick up, and export orders are forecast to remain the same. Small and large companies are forecasting positive figures for most measurements. Medium companies are forecasting decreases in UK order intake, export orders and employee numbers.

Non-metal products is the only sector forecasting that the next quarter will be better than the previous. Mechanical equipment are expecting a decrease in output; machine shops are expecting a decrease in export orders; fabricators are forecasting a decrease in both UK and export orders; electronics and metal manufacturing are expecting decreases in UK and export orders, export prices and employee. numbers, with metal manufacturing also forecasting a decrease in output volume.

| Net | Up | Same | Down | |

Orders | 12% | 36% | 40% | 24% |

UK Orders | 4% | 30% | 44% | 26% |

Export Orders | 0% | 23% | 54% | 23% |

Output Volume | 5% | 30% | 45% | 25% |

Balance of change %

| Order Intake UK | Orders Export | Prices UK | Prices Export | Output Volume | Employees | |

|---|---|---|---|---|---|---|

| Small | 2 | 0 | 12 | 9 | 3 | 13 |

| Medium | -4 | -13 | 8 | 4 | 8 | -4 |

| Large | 75 | 75 | 25 | 25 | 25 | 50 |

| Metal Manufacturing | -13 | -43 | 0 | -14 | -25 | -13 |

| Non-Metal Products | 14 | 33 | 29 | 17 | 14 | 0 |

| Electronics | -33 | -20 | 0 | -20 | 0 | -33 |

| Fabricators | -15 | -43 | 0 | 0 | 8 | 0 |

| Machine Shops | 13 | -17 | 25 | 17 | 13 | 25 |

| Mechanical Equipment | 13 | 4 | 9 | 18 | -4 | 24 |